The global SaaS industry continues to demonstrate robustness and resilience regarding an agitated geopolitical situation, while experiencing a growing importance within the software ecosystem. In 2024, the market was valued at approximatively $399Bn, and forecasts suggest that it will more than double by the end of the decade, reaching $820Bn by 2030. This trajectory reflects a sustained CAGR of 12%, underscoring investor confidence and market resilience even in the face of macroeconomic uncertainty.

SaaS now accounts for a substantial proportion of global enterprise software spending. North America remains the dominant region, representing 43% of total revenue, while the CRM segment stands out as the industry’s largest contributor, accounting for over 84% of global SaaS revenue. This disproportionate concentration reveals a broader trend toward deepening verticalization and enterprise-specific solutions, with CRM and private cloud platforms continuing to consolidate their role at the center of enterprise IT stacks.

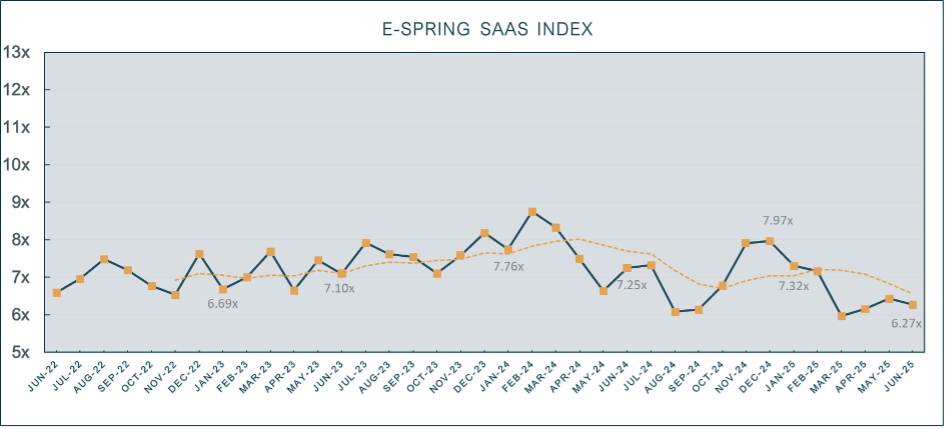

The E-Spring B2B SaaS Index recorded a marked decline over the first half of 2025, reflecting broader market turbulence and geopolitical uncertainty. Valuations dropped from 7.97x in December 2024 to 5.9x in March 2025, before showing a modest rebound to 6.27x EV/Sales by the end of June 2025.

This downward trajectory aligns closely with global equity market contractions, largely driven by escalating US-led tariff conflicts and mounting geopolitical and economic instability. While a brief recovery emerged in April and May, optimism was short-lived. The resurgence was decisively curtailed by the renewed intensification of armed conflicts in the Middle East, which once again weighed heavily on investor sentiment and SaaS multiples.

Valuation Trends and M&A Activity

2024 was marked by a notable resurgence in SaaS-related mergers and acquisitions. A total of 2,107 transactions were recorded across the year, with SaaS accounting for 61% of all software M&A activity. This surge in consolidation reflects both a revaluation of private assets after the 2022-2023 correction, and an increasing willingness among incumbents to buy growth, innovation, and distribution channels inorganically.

Investors rewarded companies that demonstrated strong customer retention and resilient growth. The median EV/Sales multiple for high-retention SaaS companies reached 11.7x. The top-performing quartile of public SaaS stocks saw their share prices increase by 26.6% over the course of the year.

Perhaps the most profound structural transformation currently reshaping the SaaS sector is the ongoing shift in pricing strategies. For over a decade, the dominant model for monetization in SaaS has been based on a “per seat” pricing, charging customers according to the number of users on the platform, typically through monthly or annual licenses.

Shifting Pricing Models in the Age of AI

AI and Machine Learning are playing an increasingly important role with projections indicating that 60% of SaaS platforms will integrate AI by 2025. However, the rise of AI has introduced new complexities. The integration of AI into SaaS platforms, particularly generative models and inference-heavy workloads, has significantly increased the variability of compute costs. This has made the traditional licensing model less economically aligned with usage, particularly for companies offering compute-intensive services.

In response, a growing number of SaaS vendors are pivoting toward usage-based or pay-as-you-go pricing models. These models, long used by cloud infrastructure providers, offer closer alignment between customer value and cost, rewarding companies that deliver higher engagement or processing efficiency. Usage-based pricing also allows customers to scale more fluidly, adjusting their spending in real time based on their evolving needs.

Tariffs and their implications for the SaaS industry

Tariffs have minimal direct impact on SaaS companies due to their digital, borderless nature. Since most SaaS products are delivered via cloud-based subscriptions, they typically fall outside traditional tariff regimes designed for physical goods. However, indirect effects such as economic uncertainty from trade policies can lead to longer sales cycles and cautious customer spending. SaaS businesses relying on global infrastructure or outsourced services may face increased costs if tariffs affect these areas. Despite these challenges, the inherent resilience of the SaaS model, characterized by recurring revenues and essential services, helps mitigate the broader impacts of tariff-induced market volatility.

Conclusion

Despite ongoing geopolitical tensions and market volatility, the global SaaS sector remains resilient, with strong fundamentals and a projected CAGR of 12% through 2030. While valuations declined in early 2025 to 6.27x EV/Sales, investor confidence persists, reflected in robust M&A activity and a pivot toward usage-based pricing models amid rising AI adoption. As SaaS becomes increasingly embedded in enterprise IT, its recurring revenues and scalable delivery continue to offer stability in an uncertain macroeconomic landscape.

Written by Nicolas Delronge

References:

- Business Insiders. (2025, April 24). AI is changing how software companies charge customers. Welcome to the pay-as-you-go future. Business Insider. https://www.businessinsider.com/saas-ai-changing-how-software-companies-charge-customers-2025-4

- Software Equity Group. (2025, February 21). SEG 2025 Annual SAAS Report. https://www.softwareequity.com/research/annual-saas-report

- Software as a Service Market Size | Industry Report, 2030. (n.d.). https://www.grandviewresearch.com/industry-analysis/saas-market-report

- Sullivan, D. (2025, June 9). Multiples SaaS 2025: Guide complet des mesures d’évaluation et des critères de référence – Flippa. https://flippa.com/blog/fr/multiples-saas-2025/

- How tariffs Impact SaaS: The Borderless Edge in Tech M&A | L40° Insights. (n.d.). https://www.l40.com/insights/tariff-impact-m-a